Bu strateji burada yer alan Capissimo adlı kullanıcının 'Machine Learning: kNN-based Strategy' adlı göstergesi esas alınarak hazırlanmıştır.

'Machine Learning: kNN-based Strategy' adlı gösterge ile ilgili olarak yazarı tarafından yapılan açıklamanın Türkçesi aşağıdadır:

Bu strateji, bir sonraki (yarın, gelecek ay, vb.) piyasa hareketi için bir tahmin elde etmenizi sağlamak üzere klasik bir makine öğrenimi algoritması (k En Yakın Komşular (kNN)) kullanır. Denetimsiz bir makine öğrenme algoritması olan kNN, en basit öğrenme algoritmalarından biridir.

Bir sonraki piyasa hareketinin tahminini yapmak için kNN algoritması, 3 dizide (feature1, feature2 ve directions) toplanan geçmiş verileri kullanır ve mevcut gösterge(ler) değerlerinin k-en yakın komşularını bulur.

İki boyutlu kNN algoritması, geçmişte iki göstergenin benzer seviyede olduğu zamanlarda neler olduğuna bir göz atıyor. Daha sonra en yakın k komşuya bakar, durumlarını görür ve böylece mevcut noktayı sınıflandırır.

KNN algoritması, herhangi bir *tahmin değeri* olup olmadığını görmek için her türlü göstergeyi kolayca test etmek için bir çerçeve sunar.

Uyarı: Sinyaller yeniden boyama yapabilir!

Strateji dahilinde, stratejiye ait ön tanımlı değerler değiştirilebilir:

Esas alınan gösterge değerleri ile ilgili yapılabilecek değişiklikler

Strateji ile ilgili yapılabilecek değişiklikler

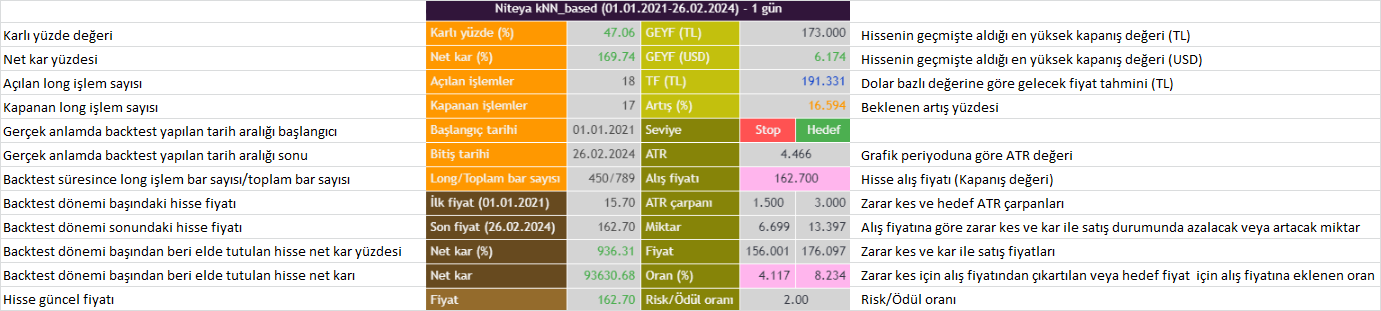

Aşağıdaki grafikte, stratejiyi yüklediğimizde ekrana gelecek olan tablonun değerleri ve açıklamaları gösterilmektedir:

Stratejinin temel değerleri ve anlamları aşağıda gösterilmektedir:

Bu ayarlar, stratejinin "Ayarlar/Özellikler" sekmesinde değiştirilebilir.

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © Niteya

//@version=5

// Bu strateji https://tr.tradingview.com/v/GpcT4M6T/ adresindeki Capissimo adlı kullanıcının 'Machine Learning: kNN-based Strategy' adlı göstergesi esas alınarak hazırlanmıştır.

// Bu strateji şablonu sadece eğitim amaçlı olarak verilmiştir. Yatırım kararlarınızda kullanmayınız.

strategy("Niteya Strategy kNN-based", shorttitle='Niteya kNN-based', overlay=true, calc_on_every_tick=true, commission_value=0.04, initial_capital=10000, default_qty_type=strategy.cash, default_qty_value=10000)

////////////////////////////////////////////

Indicator = input.string('All', 'Indicator', ['RSI','ROC','CCI','Volume','All'])

ShortWindow = input.int(14, 'Short Period [1..n]', 1)

LongWindow = input.int(28, 'Long Period [2..n]', 2)

BaseK = input.int (252, 'Base No. of Neighbours (K) [5..n]', 5)

Filter = input.bool (false, 'Volatility Filter')

Bars = input.int (300, 'Bar Threshold [2..5000]', 2, 5000)

show_labels = input.bool (true, 'Show labels')

// Backtest period

StartYear = input(2021, 'Backtest start year')

StartMonth = input(1, 'Backtest start month')

StartDay = input(1, 'Backtest start day')

PeriodStart = timestamp(StartYear, StartMonth, StartDay, 0, 0)

StopYear = input(9999, 'Backtest stop year')

StopMonth = input(12, 'Backtest stop month')

StopDay = input(31, 'Backtest stop day')

PeriodStop = timestamp(StopYear, StopMonth, StopDay, 0, 0)

// Constants

var int BUY = 1

var int SELL = -1

var int CLEAR = 0

var int k = math.floor(math.sqrt(BaseK)) // k Value for kNN algo

// Variable

// Training data, normalized to the range of [0,...,100]

var array<float> feature1 = array.new_float(0) // [0,...,100]

var array<float> feature2 = array.new_float(0) // ...

var array<int> directions = array.new_int(0) // [-1; +1]

// Result data

var array<int> predictions = array.new_int(0)

var float prediction = 0.0

var array<int> bars = array.new<int>(1, 0) // array used as a container for inter-bar variables

// Signals

var int signal = CLEAR

// Functions

minimax(float x, int p, float min, float max) =>

float hi = ta.highest(x, p), float lo = ta.lowest(x, p)

(max - min) * (x - lo)/(hi - lo) + min

cAqua(int g) => g>9?#0080FFff:g>8?#0080FFe5:g>7?#0080FFcc:g>6?#0080FFb2:g>5?#0080FF99:g>4?#0080FF7f:g>3?#0080FF66:g>2?#0080FF4c:g>1?#0080FF33:#00C0FF19

cPink(int g) => g>9?#FF0080ff:g>8?#FF0080e5:g>7?#FF0080cc:g>6?#FF0080b2:g>5?#FF008099:g>4?#FF00807f:g>3?#FF008066:g>2?#FF00804c:g>1?#FF008033:#FF008019

//-- Logic

// 3 pairs of predictor indicators, long and short each

float rs = ta.rsi(close, LongWindow), float rf = ta.rsi(close, ShortWindow)

float cs = ta.cci(close, LongWindow), float cf = ta.cci(close, ShortWindow)

float os = ta.roc(close, LongWindow), float of = ta.roc(close, ShortWindow)

float vs = minimax(volume, LongWindow, 0, 99), float vf = minimax(volume, ShortWindow, 0, 99)

float f1 = switch Indicator

'RSI' => rs

'CCI' => cs

'ROC' => os

'Volume' => vs

=> math.avg(rs, cs, os, vs)

float f2 = switch Indicator

'RSI' => rf

'CCI' => cf

'ROC' => of

'Volume' => vf

=> math.avg(rf, cf, of, vf)

// Classification data, what happens on the next bar

int class_label = int(math.sign(close[1] - close[0]))

In_Period() =>

time >= PeriodStart and time <= PeriodStop ? true : false

// Use particular training period

if In_Period()

// Store everything in arrays. Features represent a square 100 x 100 matrix,

// whose row-colum intersections represent class labels, showing historic directions

array.push(feature1, f1)

array.push(feature2, f2)

array.push(directions, class_label)

// Core logic of the algorithm

int size = array.size(directions)

float maxdist = -999.0

// Loop through the training arrays, getting distances and corresponding directions.

if size>0

for i=0 to size-1

// Calculate the euclidean distance of current point to all historic points,

// here the metric used might as well be a manhattan distance or any other.

float d = math.sqrt(math.pow(f1 - array.get(feature1, i), 2) + math.pow(f2 - array.get(feature2, i), 2))

if d > maxdist

maxdist := d

if array.size(predictions) >= k

array.shift(predictions)

array.push(predictions, array.get(directions, i))

// Get the overall prediction of k nearest neighbours

prediction := array.sum(predictions)

atr_10 = ta.atr(10)

atr_40 = ta.atr(40)

bool filter = Filter ? atr_10 > atr_40 : true // filter out by volatility or ex. ta.atr(1) > ta.atr(10)...

// Now that we got a prediction for the next market move, we need to make use of this prediction and

// trade it. The returns then will show if everything works as predicted.

// Over here is a simple long/short interpretation of the prediction,

// but of course one could also use the quality of the prediction (+5 or +1) in some sort of way, ex. for position sizing.

bool long = prediction > 0 and filter

bool short = prediction < 0 and filter

bool clear = not(long and short)

if array.get(bars, 0)==Bars // stop by trade duration

signal := CLEAR

array.set(bars, 0, 0)

else

array.set(bars, 0, array.get(bars, 0) + 1)

signal := long ? BUY : short ? SELL : clear ? CLEAR : nz(signal[1])

int changed = ta.change(signal)

bool startLongTrade = changed!=0 and signal==BUY

bool startShortTrade = changed!=0 and signal==SELL

bool clear_condition = changed!=0 and signal==CLEAR

knn_value = startLongTrade ? 1 : startShortTrade ? -1 : 0

float maxpos = ta.highest(high, 10)

float minpos = ta.lowest (low, 10)

// Visuals

plotshape(show_labels ? (startLongTrade ? minpos : na) : na, 'Buy', shape.labelup, location.belowbar, cAqua(int(prediction*5)), size=size.small) // color intensity correction

plotshape(show_labels ? (startShortTrade ? maxpos : na) : na, 'Sell', shape.labeldown, location.abovebar, cPink(int(-prediction*5)), size=size.small)

plot(show_labels ? (clear_condition ? close : na) : na, 'ClearPos', color.rgb(68, 66, 46), 4, plot.style_cross)

////////////////////////////////////////////

is_trend = input.bool(false, title="Trend gücü", inline='adx')

trend_short = input.bool(false, title="In short", inline='adx')

is_volume = input.bool(false, title="Hacim", inline='volume')

volume_short = input.bool(false, title="In short", inline='volume')

// EMA giriş değerleri

var string ema_group = 'EMA değerleri'

ema_length1 = input(20, 'EMA length1', group=ema_group)

ema_length2 = input(50, 'EMA length2', group=ema_group)

ema_length3 = input(200, 'EMA length3', group=ema_group)

is_ema_lines = input.bool(true, title='MA çizgileri', group=ema_group)

var string buy_sell_group = 'ATR temelli alış ve satış seviye değerleri'

buy_method = input.string(title='Satın alma yöntemi', defval='Kaynak', options=['Kaynak', 'Kullanıcı tanımlı'], group=buy_sell_group)

buy_src = input(close, 'Satın alma kaynağı', group=buy_sell_group)

buy_val = input.float(defval=0.00, title='Alış fiyatı', group=buy_sell_group)

atr_period_buy = input.int(14, 'ATR periyodu', minval=1, step=1, group=buy_sell_group)

atr_mul_stop = input.float(1.50, title='ATR çarpanı (Stop loss)', group=buy_sell_group)

atr_mul_target = input.float(3.00, title='ATR çarpanı (Satış)', group=buy_sell_group)

is_buy_lines = input.bool(false, title='Satın alma, stop loss ve satış seviye çizgileri', group=buy_sell_group)

// EMA

ema_11 = ta.ema(close, ema_length1)

ema_12 = ta.ema(close, ema_length2)

ema_13 = ta.ema(close, ema_length3)

plot(is_ema_lines ? ema_11 : na, title="MA src1", color=color.blue, linewidth=1)

plot(is_ema_lines ? ema_12 : na, title="MA src2", color=color.orange, linewidth=2)

plot(is_ema_lines ? ema_13 : na, title="MA src3", color=color.black, linewidth=3)

var long_vals = "Long işlem çıkış değerleri"

sl_method = input.string('Short', title="Çıkış yöntemi", options=['Stop loss', 'Short', 'Both'], group=long_vals)

// Zarar durdur için ATR giriş değerleri

atr_period = input.int(14, 'Zarar durdur ATR periyodu', minval=7, step=1, group=long_vals)

atr_multiplier = input.float(3, 'Zarar durdur ATR çarpanı', minval=1.5, step=0.1, group=long_vals)

// DMI inputs

dmi_lensig = input.int(14, title="ADX Smoothing", minval=1, maxval=50)

dmi_len = input.int(14, minval=1, title="ADX DI Length")

dmi_level = input.int(25, minval=20, title="ADX level")

up = ta.change(high)

down = -ta.change(low)

plusDM = na(up) ? na : (up > down and up > 0 ? up : 0)

minusDM = na(down) ? na : (down > up and down > 0 ? down : 0)

trur = ta.rma(ta.tr, dmi_len)

plus = fixnan(100 * ta.rma(plusDM, dmi_len) / trur)

minus = fixnan(100 * ta.rma(minusDM, dmi_len) / trur)

sum = plus + minus

adx = 100 * ta.rma(math.abs(plus - minus) / (sum == 0 ? 1 : sum), dmi_lensig)

trend_value = adx>adx[1] and adx>=dmi_level and adx>=ta.sma(adx, 10) ? 1 : 0

// Volume calculations

volume_value = (volume >= 1.1 * ta.sma(volume, 10)) ? 1 : 0

var int long_index = 0

var float long_price = 0.00

var int stop_index = 0

var float stop_val = 0.00

var int long_no = 0

var int close_no = 0

// ATR hesaplama

atr_long = ta.atr(atr_period)

// İz süren stop hesaplama

stop_loss_atr = atr_multiplier * atr_long

Trail = 0.0

iff_1 = close > nz(Trail[1], 0) ? close - stop_loss_atr : close + stop_loss_atr

iff_2 = close < nz(Trail[1], 0) and close[1] < nz(Trail[1], 0) ? math.min(nz(Trail[1], 0), close + stop_loss_atr) : iff_1

Trail := close > nz(Trail[1], 0) and close[1] > nz(Trail[1], 0) ? math.max(nz(Trail[1], 0), close - stop_loss_atr) : iff_2

ema_200 = ta.ema(close, 200)

entry_long = knn_value==1 and (not na(ema_200) ? close>ema_200 : true) and (is_volume ? volume_value==1 : true) and (is_trend ? trend_value==1 : true)

entry_short = knn_value==-1 and (volume_short ? volume_value==1 : true) and (trend_short ? trend_value==1 : true)

entry_price_long = ta.valuewhen(entry_long, close, 0)

stop_loss_long = Trail

exit_long = close<stop_loss_long

// Aktif periyot

var int PeriodS1 = 0

var int PeriodS2 = 0

if barstate.isfirst

if time >= PeriodStart

PeriodS1 := timestamp(year(time), month(time), dayofmonth(time), 0, 0)

else

PeriodS1 := timestamp(year(PeriodStart), month(PeriodStart), dayofmonth(PeriodStart), 0, 0)

if last_bar_time <= PeriodStop

PeriodS2 := timestamp(year(last_bar_time), month(last_bar_time), dayofmonth(last_bar_time), 0, 0)

else

PeriodS2 := timestamp(year(PeriodStop), month(PeriodStop), dayofmonth(PeriodStop), 0, 0)

// Hissenin periyot içindeki ilk ve son fiyatı

var float close_s = na

var float close_e = na

if time >= PeriodS1 and na(close_s[1])

close_s := close

else

close_s := close_s[1]

if time >= PeriodS2 and na(close_e[1])

close_e := close

else

close_e := close_e[1]

var int bar_number_period = 0

var int bar_number_long = 0

bar_index_o = (last_bar_index - bar_index)

if In_Period()

if entry_long and strategy.opentrades==0

strategy.entry('long', strategy.long, comment='BUY' + '(' + str.tostring(bar_index_o+1) + ')')

long_price := entry_price_long

long_index := bar_index_o

long_no += 1

if strategy.opentrades>0 and (sl_method=='Both' ? exit_long or entry_short : (sl_method=='Stop loss' ? exit_long : entry_short))

strategy.close('long', comment='SELL' + '(' + str.tostring(bar_index_o+1) + ')')

close_no += 1

stop_index := bar_index_o

stop_val := close

long_price := 0.00

long_index := 0

bar_number_period += 1

if long_price!=0.00

bar_number_long += 1

plot_con = In_Period() and strategy.position_size > 0

plot(plot_con and not exit_long ? stop_loss_long : na, style=plot.style_linebr, color=color.new(color.red, 0), linewidth=1, title='Stop loss level')

// plot(stop_loss_long, style=plot.style_linebr, color=color.new(color.red, 0), linewidth=1, title='Stop loss level')

// ATR temelli alım satım tablosu değerlerini hesaplama

price_src = buy_method=='Kaynak' ? buy_src : buy_val

atr_val_buy = ta.atr(atr_period_buy)

stop_price_decreased = atr_mul_stop * atr_val_buy

stop_price = price_src - stop_price_decreased

stop_rate = (100*stop_price_decreased)/price_src

target_price_increased = atr_mul_target * atr_val_buy

target_price = price_src + target_price_increased

target_rate = (100*target_price_increased)/price_src

GetWinRate(includeEvens = false) =>

winTradeCount = strategy.wintrades + (includeEvens ? strategy.eventrades : 0)

(winTradeCount / strategy.closedtrades) * 100

get_date(time_val) =>

str.tostring(dayofmonth(time_val), "00") + '.' + str.tostring(month(time_val), "00") + '.' + str.tostring(year(time_val)) + ' (' + str.tostring(hour(time_val), "00") + ':' + str.tostring(minute(time_val), "00") + ':' + str.tostring(second(time_val), "00") + ')'

cur_exchange = "USDTRY"

bar_number = last_bar_index+1

[close_ticker_cur, close_ticker_high_cur] = request.security(syminfo.tickerid, "D", [close[1], ta.highest(close[1], bar_number)], lookahead=barmerge.lookahead_on, currency=syminfo.currency)

[close_ticker_usd, close_ticker_high_usd] = request.security(syminfo.tickerid, "D", [close[1], ta.highest(close[1], bar_number)], lookahead=barmerge.lookahead_on, currency="USD")

usd_cur = request.security(cur_exchange, "D", close[1], lookahead=barmerge.lookahead_on) // Dollar exchange rate

var bool is_lines = false

var label label_ema1 = na

var label label_ema2 = na

var label label_ema3 = na

if barstate.islast

string time_str = ''

period = timeframe.period

gwr = GetWinRate()

text_color_wr = gwr > 0 ? color.green : gwr < 0 ? color.red : color.gray

text_color_np = strategy.netprofit > 0 ? color.green : strategy.netprofit < 0 ? color.red : color.gray

text_color_single = close_e-close_s > 0 ? color.green : close_e-close_s < 0 ? color.red : color.gray

if is_buy_lines and not is_lines

bar_past = bar_index[40]

bar_past_label = bar_index[20]

var line target_line = line.new(bar_index, target_price, bar_past, target_price, extend=extend.none, color=color.green, width=1)

var line buy_line = line.new(bar_index, price_src, bar_past, price_src, extend=extend.none, color=color.blue, width=1)

var line stop_line = line.new(bar_index, stop_price, bar_past, stop_price, extend=extend.none, color=color.red, width=1)

linefill.new(target_line, buy_line, color=color.new(#59d68f, 50))

linefill.new(buy_line, stop_line, color=color.new(#fd9292, 50))

label_target = label.new(bar_past_label, target_price, text='Target: ' + str.tostring(target_price, '0.000') + ' (%' + str.tostring(target_rate, '0.000') + ')', color=color.new(color.green, 0), style=label.style_label_center, textcolor=color.white, size=size.normal)

label_src = label.new(bar_past_label, price_src, text='Buy: ' + str.tostring(price_src, '0.000') + ' - Risk/Reward ratio: ' + str.tostring(target_rate/stop_rate, '0.00'), color=color.new(color.blue, 0), style=label.style_label_center, textcolor=color.white, size=size.normal)

label_stop = label.new(bar_past_label, stop_price, text='Stop: ' + str.tostring(stop_price, '0.000') + ' (%' + str.tostring(stop_rate, '0.000') + ')', color=color.new(color.red, 0), style=label.style_label_center, textcolor=color.white, size= size.normal)

is_lines := true

tr = syminfo.currency=='TRY'

switch

period=="1" => time_str := '1 dakika'

period=="3" => time_str := '3 dakika'

period=="5" => time_str := '5 dakika'

period=="15" => time_str := '15 dakika'

period=="30" => time_str := '30 dakika'

period=="45" => time_str := '45 dakika'

period=="60" => time_str := '1 saat'

period=="120" => time_str := '2 saat'

period=="180" => time_str := '3 saat'

period=="240" => time_str := '4 saat'

str.pos(period, "D")>=0 => time_str := '1 gün'

str.pos(period, "W")>=0 => time_str := '1 hafta'

str.pos(period, "M")>=0 => time_str := '1 ay'

var table m_table = table.new(position.bottom_right, columns=5, rows=13, bgcolor=color.rgb(212, 212, 212), border_width=1, border_color=color.white)

table.merge_cells(m_table, 0, 0, 4, 0)

table.merge_cells(m_table, 3, 1, 4, 1)

table.merge_cells(m_table, 3, 2, 4, 2)

table.merge_cells(m_table, 3, 3, 4, 3)

table.merge_cells(m_table, 3, 4, 4, 4)

table.merge_cells(m_table, 3, 6, 4, 6)

table.merge_cells(m_table, 3, 7, 4, 7)

table.merge_cells(m_table, 3, 12, 4, 12)

last_time = StopYear==9999 ? time : PeriodStop

period_start = str.tostring(dayofmonth(PeriodStart), "00") + '.' + str.tostring(month(PeriodStart), "00") + '.' + str.tostring(year(PeriodStart))

period_end = str.tostring(dayofmonth(last_time), "00") + '.' + str.tostring(month(last_time), "00") + '.' + str.tostring(year(last_time))

table.cell(m_table, 0, 0, "Niteya kNN_based (" + period_start + "-" + period_end + ")" + ' - ' + str.tostring(time_str), text_color=color.white, text_halign=text.align_center, text_size=size.normal, bgcolor=color.new(#31153a, 0))

table.cell(m_table, 0, 1, 'Karlı yüzde (%)', text_color=color.rgb(244, 244, 244), text_halign=text.align_left, text_size=size.normal, bgcolor=color.orange)

table.cell(m_table, 0, 2, 'Net kar (%)', text_color=color.rgb(244, 244, 244), text_halign=text.align_left, text_size=size.normal, bgcolor=color.orange)

table.cell(m_table, 0, 3, 'Açılan işlemler', text_color=color.rgb(244, 244, 244), text_halign=text.align_left, text_size=size.normal, bgcolor=color.orange)

table.cell(m_table, 0, 4, 'Kapanan işlemler', text_color=color.rgb(244, 244, 244), text_halign=text.align_left, text_size=size.normal, bgcolor=color.orange)

table.cell(m_table, 0, 5, 'Başlangıç tarihi', text_color=color.rgb(244, 244, 244), text_halign=text.align_left, text_size=size.normal, bgcolor=color.orange)

table.cell(m_table, 0, 6, 'Bitiş tarihi', text_color=color.rgb(244, 244, 244), text_halign=text.align_left, text_size=size.normal, bgcolor=color.orange)

table.cell(m_table, 0, 7, 'Long/Toplam bar sayısı', text_color=color.rgb(244, 244, 244), text_halign=text.align_left, text_size=size.normal, bgcolor=color.orange)

table.cell(m_table, 0, 8, 'İlk fiyat (' + str.tostring(dayofmonth(PeriodS1), "00") + '.' + str.tostring(month(PeriodS1), "00") + '.' + str.tostring(year(PeriodS1)) + ')', text_color=color.rgb(244, 244, 244), text_halign=text.align_left, text_size=size.normal, bgcolor=color.rgb(103, 74, 31))

table.cell(m_table, 0, 9, 'Son fiyat (' + period_end + ')', text_color=color.rgb(244, 244, 244), text_halign=text.align_left, text_size=size.normal, bgcolor=color.rgb(103, 74, 31))

table.cell(m_table, 0, 10, 'Net kar (%)', text_color=color.rgb(244, 244, 244), text_halign=text.align_left, text_size=size.normal, bgcolor=color.rgb(103, 74, 31))

table.cell(m_table, 0, 11, 'Net kar', text_color=color.rgb(244, 244, 244), text_halign=text.align_left, text_size=size.normal, bgcolor=color.rgb(103, 74, 31))

table.cell(m_table, 0, 12, 'Fiyat', text_color=color.rgb(244, 244, 244), text_halign=text.align_left, text_size=size.normal, bgcolor=color.rgb(148, 107, 44))

if not na(gwr)

table.cell(m_table, 1, 1, str.tostring(gwr, '0.00'), text_color=text_color_wr, text_halign=text.align_right, text_size=size.normal, bgcolor=color.rgb(212, 212, 212))

table.cell(m_table, 1, 2, str.tostring((100*strategy.netprofit)/strategy.initial_capital, '0.00'), text_color=text_color_np, text_halign=text.align_right, text_size=size.normal, bgcolor=color.rgb(212, 212, 212))

table.cell(m_table, 1, 3, str.tostring(long_no), text_color=#505050, text_halign=text.align_right, text_size=size.normal, bgcolor=color.rgb(212, 212, 212))

table.cell(m_table, 1, 4, str.tostring(strategy.closedtrades), text_color=#505050, text_halign=text.align_right, text_size=size.normal, bgcolor=color.rgb(212, 212, 212))

table.cell(m_table, 1, 5, str.tostring(dayofmonth(PeriodS1), "00") + '.' + str.tostring(month(PeriodS1), "00") + '.' + str.tostring(year(PeriodS1)), text_color=#505050, text_halign=text.align_right, text_size=size.normal, bgcolor=color.rgb(212, 212, 212))

table.cell(m_table, 1, 6, str.tostring(dayofmonth(PeriodS2), "00") + '.' + str.tostring(month(PeriodS2), "00") + '.' + str.tostring(year(PeriodS2)), text_color=#505050, text_halign=text.align_right, text_size=size.normal, bgcolor=color.rgb(212, 212, 212))

table.cell(m_table, 1, 7, str.tostring(bar_number_long) + '/' + str.tostring(bar_number_period), text_color=#505050, text_halign=text.align_right, text_size=size.normal, bgcolor=color.rgb(212, 212, 212))

np = (close_e-close_s)*(strategy.initial_capital/close_s)

table.cell(m_table, 1, 8, str.tostring(close_s, '0.00'), text_color=#505050, text_halign=text.align_right, text_size=size.normal, bgcolor=color.rgb(212, 212, 212))

table.cell(m_table, 1, 9, str.tostring(close_e, '0.00'), text_color=#505050, text_halign=text.align_right, text_size=size.normal, bgcolor=color.rgb(212, 212, 212), tooltip=str.tostring(close_e, '0.00') + ' - ' + str.tostring(volume, '0')) // volume*close

table.cell(m_table, 1, 10, str.tostring((100*np)/strategy.initial_capital, '0.00'), text_color=text_color_single, text_halign=text.align_right, text_size=size.normal, bgcolor=color.rgb(212, 212, 212))

table.cell(m_table, 1, 11, str.tostring(np, '0.00'), text_color=text_color_single, text_halign=text.align_right, text_size=size.normal, bgcolor=color.rgb(212, 212, 212))

table.cell(m_table, 1, 12, str.tostring(close, '0.00'), text_color=text_color_single, text_halign=text.align_right, text_size=size.normal, bgcolor=color.rgb(212, 212, 212))

// TL ve USD fiyat bazında fiyat tahmin tablosu

table.cell(m_table, 2, 1, 'GEYF (TL)', text_color=color.rgb(244, 244, 244), text_halign=text.align_left, text_size=size.normal, bgcolor=color.rgb(195, 192, 13), tooltip='Geçmiş en yüksek fiyat (TL)')

table.cell(m_table, 2, 2, 'GEYF (USD)', text_color=color.rgb(244, 244, 244), text_halign=text.align_left, text_size=size.normal, bgcolor=color.rgb(195, 192, 13), tooltip='Geçmiş en yüksek fiyat (USD)')

table.cell(m_table, 2, 3, 'TF (TL)', text_color=color.rgb(244, 244, 244), text_halign=text.align_left, text_size=size.normal, bgcolor=color.rgb(195, 192, 13), tooltip='Tahmini fiyat (TL)')

table.cell(m_table, 2, 4, 'Artış (%)', text_color=color.rgb(244, 244, 244), text_halign=text.align_left, text_size=size.normal, bgcolor=color.rgb(195, 192, 13))

table.cell(m_table, 3, 1, str.tostring(close_ticker_high_cur, "0.000"), text_color=color.black, text_halign=text.align_right)

table.cell(m_table, 3, 2, str.tostring(close_ticker_high_usd, "0.000"), text_color=color.green, text_halign=text.align_right)

table.cell(m_table, 3, 3, str.tostring(close_ticker_high_usd * usd_cur, "0.000"), text_color=color.rgb(3, 57, 204), text_halign=text.align_right)

table.cell(m_table, 3, 4, str.tostring(((100*close_ticker_high_usd*usd_cur)/close_ticker_cur)-100, "0.000"), text_color=color.orange, text_halign=text.align_right)

// ATR temelli alım ve satım değerleri tablosu

table.cell(m_table, 2, 5, 'Seviye', text_color=color.rgb(244, 244, 244), text_halign=text.align_left, text_size=size.normal, bgcolor=color.rgb(134, 132, 8))

table.cell(m_table, 3, 5, 'Stop', text_color=color.rgb(244, 244, 244), text_halign=text.align_center, bgcolor=color.red)

table.cell(m_table, 4, 5, 'Hedef', text_color=color.rgb(244, 244, 244), text_halign=text.align_center, bgcolor=color.green)

table.cell(m_table, 2, 6, 'ATR', text_color=color.rgb(244, 244, 244), text_halign=text.align_left, text_size=size.normal, bgcolor=color.rgb(134, 132, 8))

table.cell(m_table, 2, 7, 'Alış fiyatı', text_color=color.rgb(244, 244, 244), text_halign=text.align_left, bgcolor=color.rgb(134, 132, 8))

table.cell(m_table, 2, 8, 'ATR çarpanı', text_color=color.rgb(244, 244, 244), text_halign=text.align_left, bgcolor=color.rgb(134, 132, 8))

table.cell(m_table, 2, 9, 'Miktar', text_color=color.rgb(244, 244, 244), text_halign=text.align_left, bgcolor=color.rgb(134, 132, 8), tooltip='Stop loss fiyat hesaplaması için alış fiyatından çıkartılan veya hedef fiyat hesaplaması için alış fiyatına eklenen miktar')

table.cell(m_table, 2, 10, 'Fiyat', text_color=color.rgb(244, 244, 244), text_halign=text.align_left, bgcolor=color.rgb(134, 132, 8), tooltip='Stop loss veya hedef fiyatı')

table.cell(m_table, 2, 11, 'Oran (%)', text_color=color.rgb(244, 244, 244), text_halign=text.align_left, bgcolor=color.rgb(134, 132, 8), tooltip='Stop loss fiyat hesaplaması için alış fiyatından çıkartılan veya hedef fiyat hesaplaması için alış fiyatına eklenen oran')

table.cell(m_table, 2, 12, 'Risk/Ödül oranı', text_color=color.rgb(244, 244, 244), text_halign=text.align_left, bgcolor=color.rgb(134, 132, 8))

table.cell(m_table, 3, 6, str.tostring(atr_val_buy, '0.000'), text_halign=text.align_center)

table.cell(m_table, 3, 7, str.tostring(price_src, '0.000'), text_halign=text.align_center, bgcolor=color.rgb(255, 181, 237))

table.cell(m_table, 3, 8, str.tostring(atr_mul_stop, '0.000'), text_halign=text.align_center)

table.cell(m_table, 3, 9, str.tostring(stop_price_decreased, '0.000'), text_halign=text.align_right, tooltip=str.tostring(atr_mul_stop, '0.000') + ' * ' + str.tostring(atr_val_buy, '0.000'))

table.cell(m_table, 3, 10, str.tostring(stop_price, '0.000'), text_halign=text.align_right, tooltip=str.tostring(price_src, '0.000') + ' - ' + str.tostring(stop_price_decreased, '0.000'))

table.cell(m_table, 3, 11, str.tostring(stop_rate, '0.000'), text_halign=text.align_right, bgcolor=color.rgb(255, 181, 237), tooltip='(100 * ' + str.tostring(stop_price_decreased, '0.000') + ') / ' + str.tostring(price_src, '0.000'))

table.cell(m_table, 4, 8, str.tostring(atr_mul_target, '0.000'), text_halign=text.align_right)

table.cell(m_table, 4, 9, str.tostring(target_price_increased, '0.000'), text_halign=text.align_right, tooltip=str.tostring(atr_mul_target, '0.000') + ' * ' + str.tostring(atr_val_buy, '0.000'))

table.cell(m_table, 4, 10, str.tostring(target_price, '0.000'), text_halign=text.align_right, tooltip=str.tostring(price_src, '0.000') + ' + ' + str.tostring(target_price_increased, '0.000'))

table.cell(m_table, 4, 11, str.tostring(target_rate, '0.000'), text_halign=text.align_right, bgcolor=color.rgb(255, 181, 237), tooltip='(100 * ' + str.tostring(target_price_increased, '0.000') + ') / '+ str.tostring(price_src, '0.000'))

table.cell(m_table, 3, 12, str.tostring(target_rate/stop_rate, '0.00'), text_halign=text.align_center, tooltip=str.tostring(target_rate, '0.00') + ' / ' + str.tostring(stop_rate, '0.00'))

if is_ema_lines

label.delete(label_ema1)

label.delete(label_ema2)

label.delete(label_ema3)

label_ema1 := label.new(x=bar_index+2, y=ema_11, text=str.tostring(ema_length1), color=color.blue, style=label.style_label_center, textcolor=color.white, size=size.small)

label_ema2 := label.new(x=bar_index+2, y=ema_12, text=str.tostring(ema_length2), color=color.orange, style=label.style_label_center, textcolor=color.white, size=size.small)

label_ema3 := label.new(x=bar_index+2, y=ema_13, text=str.tostring(ema_length3), color=color.black, style=label.style_label_center, textcolor=color.white, size=size.small)

Yukarıdaki strateji ile ilgili bir uygulama aşağıdaki grafikte gösterilmektedir: